Gaurav Keswani

Gaurav Keswani

KEY HIGHLIGHTS

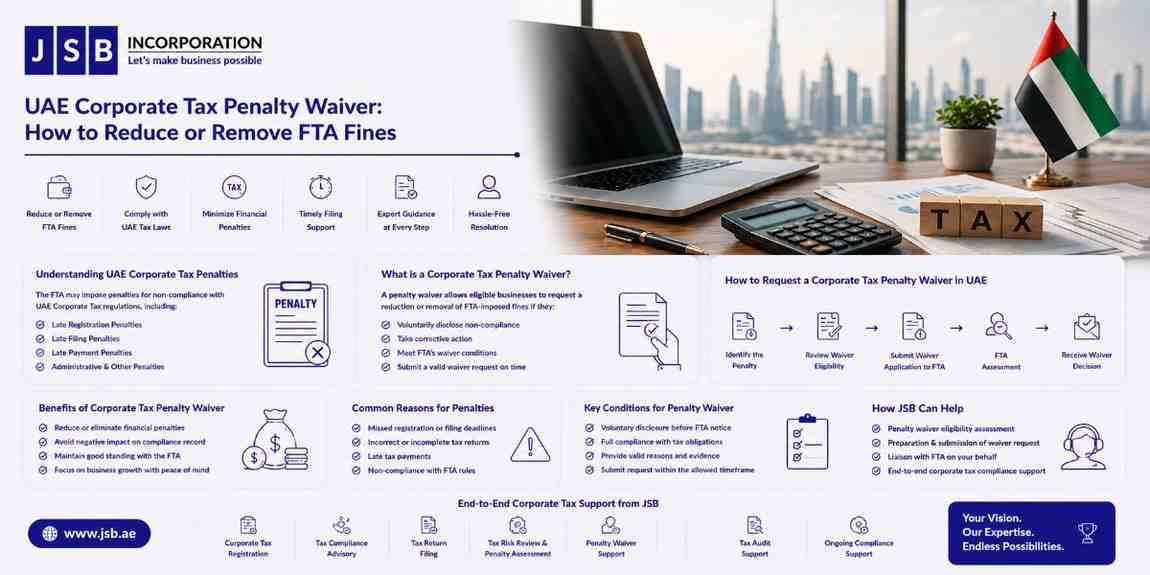

A missed corporate tax registration deadline can trigger an automatic AED 10,000 penalty under Cabinet Decision No. 75 of 2023. This penalty applies uniformly regardless of company size, activity, or jurisdiction within the UAE.

The Federal Tax Authority (FTA) has since confirmed a specific waiver pathway through Corporate Tax Public Clarification CTP006, first issued in May 2025 and updated in June 2025.

This clarification gives eligible businesses a defined route to remove or recover the penalty without lengthy disputes. It replaced years of uncertainty where businesses had no clear mechanism beyond a general reconsideration request.

This article explains exactly who qualifies for a corporate tax penalty waiver in the UAE. Keep reading the article to learn more.

TL;DR: The FTA automatically waives or refunds the AED 10,000 late corporate tax registration penalty for businesses that file their first tax return within a specific window. Other penalties can be challenged through a formal reconsideration request.

TL;DR: A corporate tax penalty waiver removes or credits back an administrative fine, most commonly the AED 10,000 late registration penalty, once specific FTA conditions are met.

The Federal Tax Authority’s CTP006 clarification applies to Taxable Persons and specific categories of Exempt Persons who missed the corporate tax registration deadline set under Federal Decree-Law No. 47 of 2022. This law forms the legal basis for the entire corporate tax regime, including its penalty structure.

Under this initiative, the FTA automatically waives the penalty if it remains unpaid. If the penalty was already settled, the FTA credits AED 10,000 back to the business’s EmaraTax account rather than issuing a manual refund through a separate process.

The relief applies to eligible late registration penalties, provided the business meets the filing condition explained below. There’s no separate application form required for this specific waiver.

The adjustment happens automatically once the return is filed within the required timeframe, which removes an administrative step many business owners assume they need to chase manually through EmaraTax support.

Knowing which pathway applies to your notice, automatic waiver versus formal reconsideration, determines how quickly your case resolves and whether you need professional support to build a case at all.

The primary category covered under CTP006 is the late corporate tax registration penalty. Businesses that registered late but file their first tax return, or annual declaration if exempt, within seven months of their first tax period’s end qualify for the waiver or refund, according to the Federal Tax Authority.

This is two months earlier than the standard nine-month filing deadline that applies to tax payment obligations. The distinction matters because many businesses confuse their payment deadline with the earlier waiver-qualifying filing deadline and miss the shorter window entirely.

Tax groups filing collectively within this seven-month window can have the penalty waived for each member’s first tax period, not just the parent entity. This group-level relief was a deliberate design choice by the FTA to avoid penalizing subsidiary entities separately when the parent group files correctly.

Exempt Persons, including qualifying investment funds and public benefit entities, follow a parallel rule based on their annual declaration deadline rather than a standard tax return. The seven-month principle still applies, measured from the end of their financial year.

Many business owners assume a penalty notice is final the moment it’s issued. It isn’t. The Federal Tax Authority built the CTP006 mechanism because many late registrations during the early corporate tax rollout stemmed from genuine unfamiliarity with a new regime, not deliberate non-compliance.

Businesses that assume nothing can be done often miss a refund or credit they already qualify for. Checking your EmaraTax account after filing confirms whether the adjustment was applied, since the process runs in the background without a confirmation email in every case.

Another common misunderstanding involves timing. Some businesses believe filing at any point after registration guarantees the waiver. In reality, the seven-month clock starts from the end of the first tax period, not from the registration date itself, and missing it by even a few days removes eligibility for the automatic adjustment entirely.

TL;DR: Confirm which waiver pathway applies to your penalty, gather the right supporting documentation, and track your exact filing deadline, since missing either window closes your options.

For penalties that fall outside the automatic CTP006 waiver, UAE tax procedure rules allow a formal reconsideration request. This must generally be submitted within 40 business days of being notified of the FTA’s decision, per the Federal Tax Authority’s published procedure.

The FTA then reviews the request within its standard review period before issuing a decision. If you disagree with the outcome or the FTA doesn’t respond in time, UAE tax procedure allows escalation to a formal dispute resolution process. All outstanding taxes and penalties must be paid first before this escalation is possible.

This requirement often surprises business owners who expect to contest a penalty without settling it, but UAE tax procedure treats payment and dispute resolution as separate tracks.

A reconsideration request needs more than a short explanation. It should include a clear, factual account of why the penalty occurred, written in a way that connects directly to the specific circumstances of your case.

Supporting evidence should include your registration timeline, prior correspondence with the FTA, or documentation proving the specific circumstance that caused the delay. Bank statements, system error screenshots, or third-party confirmations can strengthen a request when the delay was outside your direct control.

Requests lacking specific evidence, relying instead on general statements about being unaware of the deadline, rarely succeed. The FTA’s review process looks for a demonstrable, documented cause rather than a general explanation.

The 40-business-day reconsideration window starts from the date you’re formally notified of the FTA’s decision, not the date the original penalty was issued. This distinction has caught out businesses that count from the wrong starting point and submit their request too late.

For the CTP006 automatic waiver, your relevant deadline is seven months from your first tax period’s end date. These are two entirely separate clocks governing two entirely separate relief mechanisms, and confusing them is one of the most common and costly mistakes business owners make.

Businesses managing both a pending registration penalty and a separate filing-related penalty sometimes need to track two different deadlines simultaneously. Missing either one narrows your available options considerably.

Requests are frequently rejected when the explanation provided is vague. A statement like “we were unaware of the deadline” without supporting context rarely satisfies the FTA’s review standard.

Documentation that doesn’t clearly match the stated reason for delay is another common cause. If your explanation cites a banking delay but no banking correspondence is attached, the mismatch weakens the entire submission.

Requests submitted after the 40-business-day window has closed are rejected outright, regardless of how strong the underlying case might otherwise be. Weak or incomplete submissions rarely get a second chance, which makes getting the first submission right essential.

TL;DR: JSB Incorporation’s in-house Chartered Accountants review your penalty notice, confirm which waiver or reconsideration pathway applies, and manage the submission on your behalf.

They confirm your exact filing deadline based on your specific tax period, prepare the required documentation, and track your EmaraTax account to verify any eligible credit or refund has actually been applied. This structured review reduces the risk of a missed deadline or a rejected request caused by incomplete evidence.

If you’re unsure whether your penalty qualifies under current UAE corporate tax rules or a recent administrative update, a compliance review clarifies your exact position before you submit anything to the FTA.

The process starts with a review of your penalty notice and registration history. This establishes the exact category of penalty and which relief mechanism applies to it.

This is followed by identification of the correct waiver or reconsideration pathway, based on your specific tax period and filing history. Not every case follows the same route, so this step determines the entire strategy going forward.

The process ends with a documented submission through the EmaraTax portal within the FTA’s required timeframe, supported by the evidence gathered during the review stage.

Resolving the current penalty is only half the picture. Tracking your ongoing corporate tax filing obligations on a structured calendar prevents the same registration gap from resurfacing in a future tax period.

This calendar should cover registration renewals, return deadlines, and documentation updates specific to your tax period end date. Businesses with multiple entities or group structures benefit particularly from this kind of centralized tracking.

A forward calendar also flags upcoming deadlines well before they become urgent, giving your team enough lead time to gather documentation rather than scrambling in the final days before a filing window closes.

If your penalty qualifies under the FTA’s CTP006 clarification, no separate request is needed once you file your first tax return within seven months of your first tax period’s end. For other penalties requiring formal reconsideration, you generally have 40 business days from the FTA’s decision to submit your request.

2. Does the automatic waiver apply to every corporate tax penalty?

No. The automatic waiver under CTP006 applies specifically to the AED 10,000 late registration penalty for the first tax period, according to the Federal Tax Authority.

Other penalty types, such as late filing or incorrect return submissions, require a separate reconsideration request rather than qualifying for automatic relief.

3. Can a rejected reconsideration request be resubmitted?

A rejected request typically moves to formal escalation rather than direct resubmission to the FTA. Any outstanding taxes and penalties must be settled before that escalation can proceed.

4. Is the AED 10,000 late registration penalty always waived automatically?

No. The waiver only applies if you file your first tax return, or annual declaration if exempt, within seven months of your first tax period’s end. Filing later than this window means the standard penalty remains payable, and a formal reconsideration request becomes the only remaining option.

5. What happens if I already paid the penalty before the waiver was introduced?

If your penalty meets the eligible filing condition, the FTA credits the AED 10,000 directly to your EmaraTax account rather than issuing a separate cash refund. This credit can typically be applied against future tax liabilities.

6. Do tax groups need to file separately to qualify for the waiver?

No. Tax groups filing a collective return within the seven-month window can have the penalty waived for each member’s first tax period, provided the group return itself is filed on time.

A penalty notice doesn’t have to be the final outcome. Resolving it correctly depends entirely on which FTA pathway applies to your specific case and how much time remains on your deadline.

Confirming whether you qualify for the automatic CTP006 waiver or need to file a formal reconsideration request changes what you should do next. Getting this wrong, or missing either deadline, can close off your options permanently and leave the penalty standing.

If you’re also considering business setup in Dubai alongside resolving an existing compliance issue, addressing the penalty first keeps your business record clean for future registrations.

Office 2505, 25th Floor, Regal Tower, Business Bay, Dubai, UAE P.O Box 27614.

+971 4 824 4842

info@jsbincorporation.com