Gaurav Keswani

Gaurav Keswani

Key Highlights

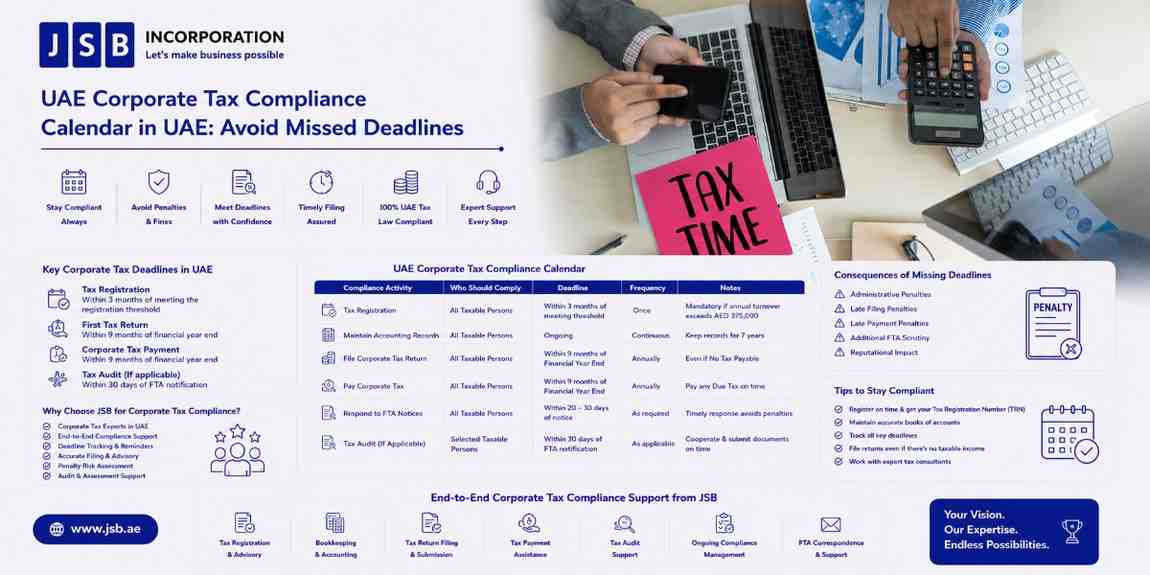

The Federal Tax Authority requires corporate tax returns and payment within nine months of the end of the relevant tax period. A calendar that treats every obligation as one annual deadline can overlook VAT periods, trade licence expiry, and action needed after a change in your business.

Corporate tax compliance calendar in the UAE should reflect your company’s tax period, assigned VAT period, trade licence expiry, and changes to its legal or operational status.

This guide helps you identify the deadlines and events that need professional review before they become a compliance issue.

A reliable compliance calendar is specific to your entity. It combines Federal Tax Authority tax deadlines with VAT periods, trade licence monitoring, and business events that can affect your compliance position.

A corporate tax compliance calendar in the UAE is an entity-specific schedule that records your corporate tax period, assigned VAT tax period, trade licence expiry, and Economic Substance Regulations position where relevant.

It should also flag inactivity, deregistration, business closure, and company-detail changes for a professional compliance review.

The Federal Tax Authority links your corporate tax return and payment deadline to the end of the relevant tax period. For taxable persons, the return and any payable corporate tax are generally due within nine months after that period ends.

Your calendar should record the entity’s financial year-end, return deadline, payment deadline, accounting-record status, and changes that affect its tax registration or filing position. This provides a clear basis for reviewing corporate tax compliance before the deadline approaches.

The Federal Tax Authority assigns a VAT tax period to each registered business. VAT returns and related payments are generally due within 28 days after the assigned period ends.

Your VAT calendar should follow the reporting period in your Federal Tax Authority account rather than a generic quarterly date list. The assigned tax period determines the deadline that applies to your business.

Your trade licence renewal timeline follows the expiry date and requirements set by the authority that issued the licence. A mainland company and a free zone company can therefore have different renewal processes and documentation requirements.

Your calendar should flag the licence expiry early enough to review business activities, shareholder details, address records, and any related government documentation. This reduces the risk of finding a required amendment only when the renewal process has already started.

A compliance provider should map obligations to your specific entity rather than provide a generic date list. The review should cover recurring filing cycles and business events that create separate compliance actions.

Corporate tax and VAT do not automatically follow the same calendar. Corporate tax follows your relevant tax period, while VAT follows the tax period assigned by the Federal Tax Authority.

A compliance review connects these deadlines with your accounting records, registrations, and trade licence status. It helps you determine whether the calendar still reflects the company you operate today.

A generic deadline list often misses the more important compliance question: what changes when your company’s operating position changes? That’s where an event-based review becomes necessary.

Inactivity, business cessation, deregistration, licence cancellation, shareholder amendments, address changes, and updates to tax records can each require a separate assessment. Fixed obligations follow a reporting period, while event-triggered actions follow a change in the business itself.

The Federal Tax Authority requires taxable persons to retain records that support their corporate tax position. Your compliance calendar should therefore reflect company changes that affect those records, registrations, or future filing requirements.

Economic Substance Regulations should not appear as a generic annual filing item for every UAE company. The Ministry of Finance announced the cancellation of ESR notification and reporting requirements for financial years ending after 31 December 2022.

However, historical exposure can still require review where a business had a relevant earlier period, an unresolved matter, or a request from the relevant authority. Your calendar should identify historical ESR exposure instead of assuming that every company has a current annual ESR filing deadline.

JSB Incorporation provides corporate tax registration and compliance support, VAT registration and compliance support, accounting, bookkeeping, company renewal support, amendments, and PRO services.

This gives your business a structured point of review for recurring deadlines and event-based compliance actions.

JSB Incorporation reviews the tax periods, records, registrations, and filing position that apply to your company. The Federal Tax Authority administers UAE corporate tax and VAT obligations, so a calendar review should align your internal records with the deadlines and periods shown in your authority account.

This approach helps identify whether your corporate tax and VAT calendar reflects the business’s current financial year, assigned VAT period, and operational status. It also creates a clearer basis for ongoing accounting and bookkeeping support.

A company amendment can affect more than the trade licence. Changes to activities, shareholders, address details, business status, or registrations can require coordinated updates across tax records, licence records, and authority submissions.

JSB Incorporation supports company renewals, amendments, PRO services, corporate tax compliance, and VAT compliance. Reviewing these elements together helps distinguish routine deadlines from actions triggered by a business change.

A UAE compliance calendar combines corporate tax deadlines, assigned VAT periods, relevant historical ESR checks, and trade licence expiry monitoring. It should also flag inactivity, closure, deregistration, and changes to company details because these events can create obligations outside the normal filing cycle.

UAE tax regulations are subject to change. Verify current requirements directly with the Federal Tax Authority or consult a qualified tax advisor for your specific situation.

1. When is corporate tax due in the UAE?

The Federal Tax Authority requires taxable persons to submit a corporate tax return and settle payable corporate tax within nine months of the end of the relevant tax period. Your deadline follows your company’s financial year-end rather than a universal date for every UAE business.

2. Is every UAE VAT return due on the same date?

No. The Federal Tax Authority assigns a VAT tax period to each registered business. VAT returns and related payments are generally due within 28 days after the assigned period ends, so the deadline shown in your Federal Tax Authority account takes priority over a generic quarterly calendar.

3. Do UAE businesses still need to file ESR reports every year?

The Ministry of Finance cancelled Economic Substance Regulations notification and reporting requirements for financial years ending after 31 December 2022. A historical review remains relevant if your business had earlier ESR exposure, an unresolved filing matter, or an authority request.

4. What happens if my UAE company has no activity?

No activity does not automatically settle your corporate tax, VAT, trade licence, or deregistration position. A professional review can assess your registrations, records, tax status, trade licence validity, and cessation position before inactivity is treated as the end of your compliance obligations.

5. How early should I review my trade licence expiry?

Your review timeline should follow the expiry date on your trade licence and the requirements of the issuing authority. Start early enough to identify whether activity, shareholder, address, or record changes need coordination before the renewal process begins.

A calendar based only on annual dates can leave material gaps in your compliance position.

Tracking corporate tax and VAT periods alongside changes such as inactivity, deregistration, amendments, and trade licence expiry gives you a more complete view of what needs attention.

Office 2505, 25th Floor, Regal Tower, Business Bay, Dubai, UAE P.O Box 27614.

+971 4 824 4842

info@jsbincorporation.com